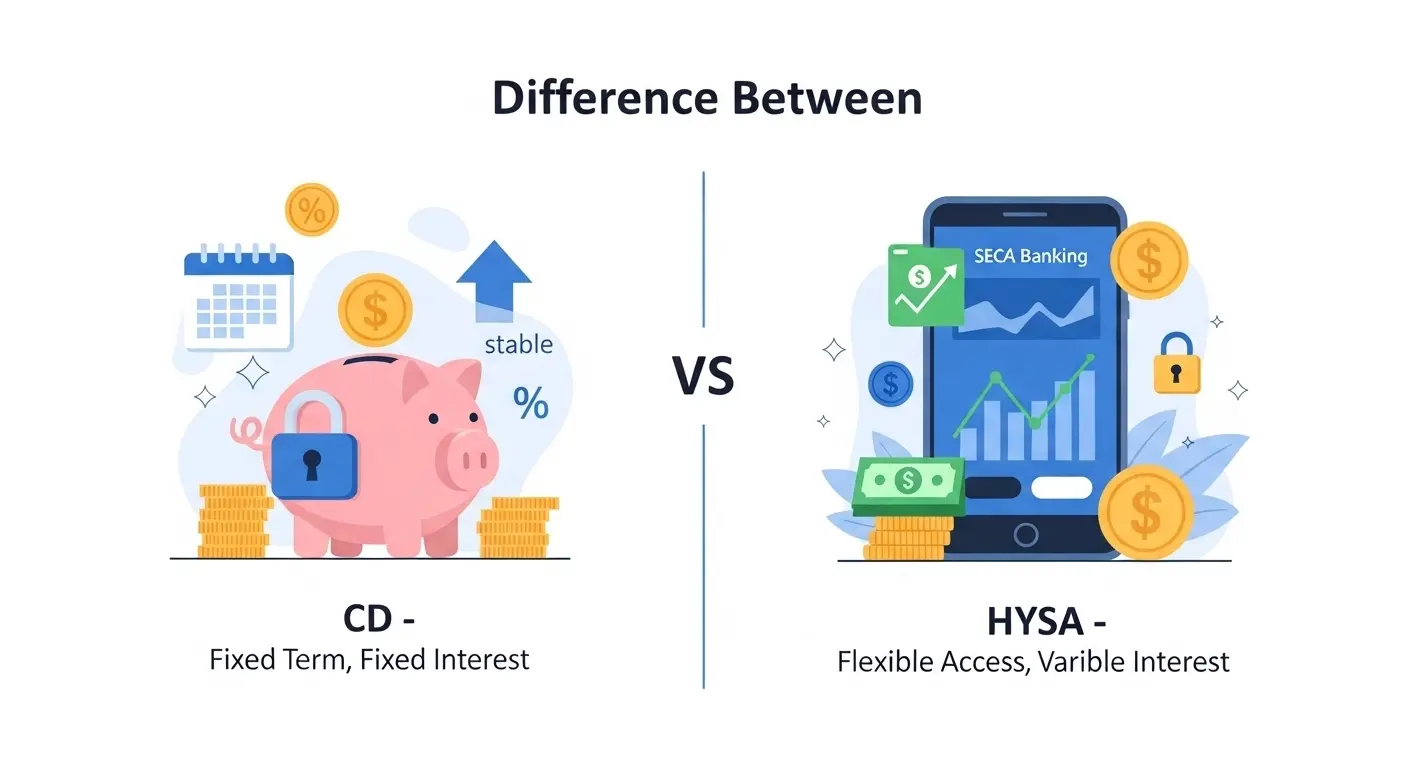

A few months ago, Ali in Lahore wanted to save money for his sister’s wedding. His bank offered him two options: a Certificate of Deposit (CD) and a High-Yield Savings Account (HYSA). He was confused about the difference between CD and HYSA. Both seemed safe. Both earned interest. But which one was better?

The difference between CD and HYSA matters because each option works differently. A CD locks your money for a fixed time. A HYSA allows flexible withdrawals. Many people search for the difference between CD and HYSA because they want better returns without risking their savings. Understanding the difference between CD and HYSA helps you make smarter financial decisions.

Before we dive deeper, let’s understand how these two savings tools truly differ.

Key Difference Between the Both

The main difference between CD and HYSA is flexibility versus commitment.

- A CD (Certificate of Deposit) requires you to lock your money for a fixed term (like 6 months or 1 year).

- A HYSA (High-Yield Savings Account) allows you to withdraw money anytime without penalties.

Why Is Their Difference Necessary to Know for Learners and Experts?

Understanding the difference is important because:

- It helps beginners manage emergency funds wisely.

- Experts use CDs for stable, predictable returns.

- It supports financial stability in society.

- It encourages smart saving habits.

- It prevents penalties caused by early withdrawals.

Financial awareness improves economic health for individuals and communities.

Pronunciation (US & UK)

CD (Certificate of Deposit)

- US: /ˌsiː ˈdiː/

- UK: /ˌsiː ˈdiː/

HYSA (High-Yield Savings Account)

- US: /ˌeɪtʃ waɪ ɛs ˈeɪ/

- UK: /ˌeɪtʃ waɪ ɛs ˈeɪ/

Now, let’s explore the detailed comparison.

Difference Between CD and HYSA

1. Lock-in Period

CD:

Money is locked for a fixed term.

Example 1: You invest for 1 year and cannot withdraw without penalty.

Example 2: A 6-month CD matures only after 6 months.

HYSA:

No lock-in period.

Example 1: You withdraw money anytime.

Example 2: You transfer funds instantly for emergencies.

2. Interest Rate Stability

CD:

Fixed interest rate.

Example 1: 5% for 12 months remains constant.

Example 2: Market changes do not affect your rate.

HYSA:

Variable interest rate.

Example 1: Rate may drop from 4% to 3%.

Example 2: Banks may increase rates during inflation.

3. Liquidity

CD:

Low liquidity.

Example 1: Early withdrawal penalty applies.

Example 2: Funds are inaccessible during term.

HYSA:

High liquidity.

Example 1: ATM access available.

Example 2: Online transfers anytime.

4. Risk Level

CD:

Very low risk.

Example 1: Guaranteed return.

Example 2: Protected by deposit insurance (in many countries).

HYSA:

Very low risk as well.

Example 1: Money insured.

Example 2: No market exposure.

5. Best For

CD:

Long-term savings goals.

Example 1: Wedding fund.

Example 2: Tuition savings.

HYSA:

Emergency funds.

Example 1: Medical bills.

Example 2: Sudden travel.

6. Minimum Deposit

CD:

Often requires a higher deposit.

Example 1: $1,000 minimum.

Example 2: Tier-based deposits.

HYSA:

Usually low minimum.

Example 1: $100 opening balance.

Example 2: Sometimes no minimum.

7. Withdrawal Penalty

CD:

Penalty charged.

Example 1: 3 months interest lost.

Example 2: Fee deducted.

HYSA:

No penalty.

Example 1: Free withdrawal.

Example 2: Instant transfer.

8. Interest Earnings Strategy

CD:

Best when rates are high.

Example 1: Lock rate before fall.

Example 2: Ladder strategy.

HYSA:

Best during rising rates.

Example 1: Benefit from increase.

Example 2: Adjustable returns.

9. Accessibility

CD:

Limited access.

Example 1: Must wait for maturity.

Example 2: Paper documentation sometimes needed.

HYSA:

Fully accessible online.

Example 1: Mobile banking.

Example 2: Debit card access.

10. Financial Discipline

CD:

Encourages disciplined saving.

Example 1: No impulsive withdrawal.

Example 2: Fixed saving habit.

HYSA:

Requires self-control.

Example 1: Easy spending temptation.

Example 2: Frequent access.

Nature and Behaviour of Both

CD: Stable, disciplined, predictable.

HYSA: Flexible, adaptive, liquid.

Why Are People Confused About Their Use?

- Both are savings tools.

- Both offer interest.

- Both are bank products.

- Similar low risk.

- Financial terms sound technical.

Difference and Similarity Table

| Feature | CD | HYSA | Similarity |

| Lock-in | Yes | No | Both save money |

| Interest | Fixed | Variable | Earn interest |

| Risk | Low | Low | Safe options |

| Liquidity | Low | High | Bank products |

| Penalty | Yes | No | Insured funds |

Which Is Better in What Situation?

CD (100 words)

A CD is better when you have extra money that you do not need immediately. If you are saving for a wedding, house down payment, or future tuition, a CD provides fixed returns and financial discipline. It protects you from spending money early. When interest rates are high, locking them through a CD is smart. It is ideal for long-term planners who prefer guaranteed outcomes.

HYSA (100 words)

A HYSA is better for emergency savings and short-term goals. If unexpected expenses arise, you can withdraw instantly without penalty. It works best for people who need flexibility and quick access to funds. During uncertain economic times, a HYSA offers safety with convenience. It suits individuals who want liquidity with decent interest.

Metaphors and Similes

- A CD is like a “locked treasure chest.”

- A HYSA is like a “wallet with growth power.”

- Saving in a CD is as steady as a clock.

- A HYSA flows like a river.

Connotative Meaning

CD: Positive (security, stability)

Example: “She locked her future in a CD.”

HYSA: Positive (freedom, flexibility)

Example: “His HYSA gave him breathing space.”

Idioms or Proverbs

- “Save for a rainy day” → HYSA example.

- “Don’t put all your eggs in one basket” → Use both CD and HYSA.

- “Slow and steady wins the race” → CD example.

Works in Literature

- The Wealth of Nations (Economics, Adam Smith, 1776)

- Rich Dad Poor Dad (Finance, Robert Kiyosaki, 1997)

Movies Related to Savings and Finance

- The Big Short (2015, USA)

- Wall Street (1987, USA)

Frequently Asked Questions

1. Is CD safer than HYSA?

Both are equally safe in insured banks.

2. Can I lose money on CDs?

Only if withdrawn early (penalty).

3. Does HYSA always pay higher interest?

Not always. It depends on market rates.

4. Which grows money faster?

Sometimes CD, sometimes HYSA.

5. Can I open both?

Yes, many people use both.

How Both Are Useful for Surroundings

- Promote financial stability.

- Encourage saving culture.

- Reduce economic stress.

- Support future planning.

Final Words for Both

CD represents discipline and certainty.

HYSA represents flexibility and readiness.

Conclusion

Understanding the difference between CD and HYSA helps you choose wisely based on your goals. A CD offers fixed returns and structured savings. A HYSA provides liquidity and flexibility. Both are safe and beneficial when used correctly.

Instead of choosing one blindly, align your choice with your financial needs. Smart saving is not about higher interest only — it is about strategy. When you understand the difference between CD and HYSA, you gain control over your financial future.